Historical Funding Rates: A Study, with Implications for UXD’s Insurance Fund

At its heart, the UXD stablecoin represents the “principal” position of a basis trade. By the definition of the underlying collateral position being “delta-neutral”, the $1 of principal collateral underlying the position is always worth $1, regardless of market conditions. However, this $1 in underlying principal is not the whole story: the delta-neutral position inherently generates a yield known as the “funding rate” due to the perpetual futures underlying the stablecoin.

One of the most frequent questions UXD Protocol is asked: “What have funding rates for perpetual futures looked like historically? How would the insurance fund have performed in different market regimes?”. Understanding funding rates is critical to understanding the long-term health profile of UXD as a stablecoin, as funding rates determine the probability that UXD may ever become undercollateralized.

To better understand funding rate dynamics in the context of UXD specifically, UXD wrote a academic-esque report analysing funding rates for both BTC and SOL perpetual futures. BTC has the longest historical data for any set of funding rates, with data from BitMEX going back to 2017. SOL’s rise to prominence is quite recent, and therefore historical data is more limited. That being said, UXD Protocol has included both to give a sense for how UXD’s insurance fund would have performed in either case.

See below for a summarized version of the full report with corresponding Github repo. Note that the below report assumes that 100% of the funding rate goes to the insurance fund. In actuality, it will be split between UXP holders and the insurance fund. A 50/50 split scenario can be seen in the full report.

Results-

Historical Data

In order to answer this question, UXD has collected historical data on both XBTUSD funding rates on BitMEX, as well as SOLPERP funding rates on FTX. One thing to note in the below charts is that early funding rates are incredibly volatile, and likely aren’t representative of future funding rate conditions.

It’s quite interesting to note the relative volatility of the two funding rates, with SOLPERP funding rates fluctuating within a tight range starting in the summer of 2021.

Taking a quick step back, it’s worth remembering that every stablecoin has its “point of instability”: for DAI, this is liquidation-related as well as having sufficient stableswap liquidity; for FEI, this is related to its PCV asset reserve; for UST, this is related to the reflexivity of its mint/burn of LUNA. For UXD stablecoin, the potential point of instability is the funding rate. Sustained negative funding rates that cause the insurance fund to deplete could cause UXD to become undercollateralized over time (though, users are allowed to redeem $1 of crypto collateral at any time before this happens).

What’s notable here is that UXD’s “point of instability” has the characteristics of a mean-reverting, drift-less process (see: Stationarity). Just a quick glance at the above charts makes it clear that funding rates don’t seem to “persist” from time step to time step (look at the sharp slope of the funding rate curves; a spike up or down in funding rates is almost immediately brought back towards zero). These properties are strong points for UXD’s stability. In a world with funding rates equal to zero always, UXD would achieve perfect stability. A strongly mean-reverting, drift-less process is the next best thing.

Fixed Start Date

Returning to the analysis, the first set of results comes from the question “What would the balance of the insurance fund look like if steady-state funding rates looked like 2021 funding rates?”. Assuming $500mm of UXD outstanding and adjusting for price appreciation of SOL and BTC over the same time period (it is assumed that SOL and BTC price is constant from the day 1 price*), results follow:

- A 100% SOLPERP backed UXD receiving 100% of the funding rate would have resulted in the insurance fund growing from $57mm to over $180mm in one year’s time.

- A 100% XBTUSD backed UXD receiving 100% of the funding rate would have resulted in the insurance fund growing from $57mm to over $115mm in one year’s time.

- Note this results in a very conservative estimate: since funding payments are computed as the funding rate times the price of the underlying asset, and because positive (negative) funding rates are generally associated with rising (falling) prices, a constant price assumption understates the size of positive funding payments, and overstates the size of negative funding payments.

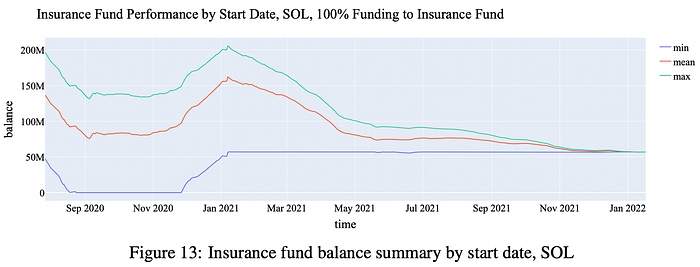

Varied Start Dates

Of course, assuming that longer-run funding rates look like they did during 2021 is a very bullish assumption, and so the performance over the entire period (2017-present) is evaluated for which funding rate data is available as follows:

Assume that UXD Protocol has $500 million of UXD stablecoin outstanding on a date “X”, what would the performance of the insurance fund have been to date? In particular what would the maximum value of the insurance fund have been since inception? the average value? the minimum value?

So for each date between (2017-present), three numbers are plotted: max, mean, min, which give an excellent sense of the insurance fund’s performance in different market regimes (bear and bull markets).

SOLPERP:

In the above, although the average performance is quite good, note that some dates show a “bankruptcy” of the insurance fund, though starting dates related to the “bankruptcy” of the insurance fund occur before Jan 2021 (i.e. before SOL had a market cap above $1bn and was considered a blue-chip crypto asset), due to the extremely high volatility of funding rates. As is clear from the SOLPERP funding chart at the beginning of this article, SOLPERP funding rate volatility has decreased significantly after achieving a $1bn+ market cap. So, UXD Protocol views these outcomes as quite unlikely moving forward but wanted to include them for completeness and transparency.

Also note that the “time to bankruptcy” in the few poor performance cases takes between several months and a year to fully deplete the insurance fund. This implies that a UXD holder would have several months opportunity to withdraw $1 of crypto assets before becoming undercollateralized.

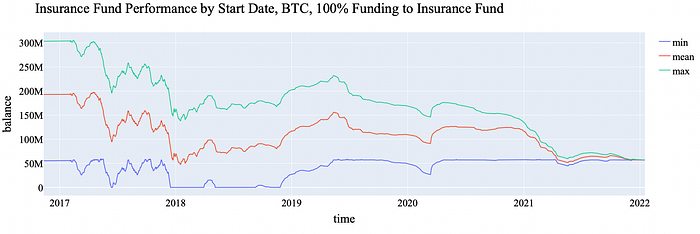

XBTUSD:

Likewise, the average performance of the BTC perp positions is quite good, with bankruptcy scenarios mostly related to the extremely volatile funding rates of 2018.

Effects of UXD Supply Caps

One thing to note about the above analysis is that is assumes $500mm of UXD stablecoin is outstanding from day 1, so it is closer to a “steady state” analysis. One of the reasons UXD Protocol decided to implement initial supply caps (beyond reasons of confirming security), was to help lessen the effects of different market regimes initially. This makes the initial launch of the protocol much more robust, as the probability of depleting the insurance fund significantly decreases. In particular, if instead it is assumed that the outstanding UXD stablecoin supply grows in-line with our proposed supply cap schedule, the insurance fund is much less likely to ever reach a “bankruptcy” scenario.

UXD Supply Cap schedule: assumes linear growth to $1bn after lifting final $200mm supply cap

Once again, the max, min, and average balance of the insurance fund according to different starting dates are shown:

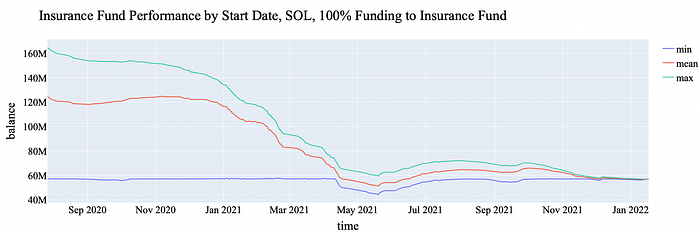

SOLPERP:

Note that the balance of the insurance fund never goes below $40mm due to the supply cap schedules, though it achieves a lower maximum value. This implies that a gradual release approach may help de-risk the initial rollout of UXD stablecoin.

XBTUSD:

Due to the volatility of XBTUSD rates in 2018 and earlier, this chart looks much the same as the $500mm constant UXD outstanding chart, so there is less of an effect to the gradual release schedule in this case.

In actuality, UXD will be a multi-collateral stablecoin with various blue-chip assets backing it, such as SOL, BTC, and ETH. The above results are meant to be demonstrations of the behaviour of funding rates historically, but do not fully reflect reality due to their simplifications. In any case, UXD Protocol believes that the above results show the robustness of the insurance fund. Although it is not guaranteed that UXD stablecoin will generate self-sustaining yield, it certainly has in most cases historically.

Effects of Insurance Fund Asset Management Returns

Finally, UXD investigated the effects of insurance fund asset management strategies on the insurance fund’s overall performance. These will include investments such as stablecoin liquidity provision, stablecoin lending, etc.

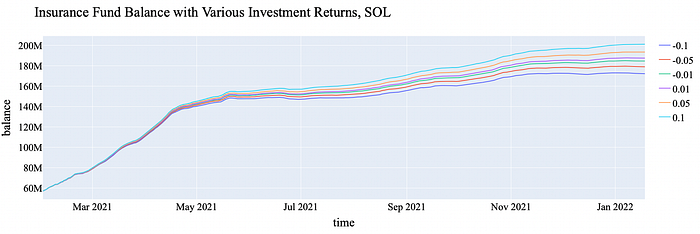

For example, a 100% SOLPERP backed UXD receiving 100% of the funding rate (with funding rates similar to 2021 regime and $500mm UXD stablecoin outstanding) with different asset management returns would have performed as follows:

Note: 0.1 = 10% constant annualized return on the assets in the insurance fund, -0.1 = -10% constant annualized return on assets in the insurance fund, with intermediate values shown.

What’s interesting about the above chart is the relative closeness of the lines, even for very different asset management performance. This implies that the primary factor in determining the insurance fund performance is funding rate, rather than asset management performance. This is not surprising, since the insurance fund has a levered exposure to funding rates. A corollary is that the asset management strategies of the insurance fund should be low-risk investments, as most of the variance in performance will come from funding rates.

If you’ve made it this far, kudos. Hopefully the above has been instructive in helping understand (i) what funding rates have been historically for two primary crypto assets (ii) why this is important for UXD Protocol (iii) how UXD Protocol’s insurance fund would have performed in different market regimes (iv) how UXD Protocol should think about managing its insurance fund.

Cheers.