UXD Protocol Fund Structure

One of the most common questions in the UXD Protocol discord is: “How will UXP governance token holders partake in the delta-neutral yield generation? What will the structure be?”. After a long design process, during which UXD Protocol explored various potential options, UXD Protocol is finally ready to propose a structure for the “Protocol Fund” that uses its recently introduced veRev mechanism. The purpose of today’s blog post is to propose a structure for community feedback, as the proposed fund will take some time to build, including the veRev mechanism.

This is going to be a long post, bear with it. Skip to “tl;dr — the Protocol Fund Structure” for the most essential info.

UXD Stakeholders

For quite some time, UXD Protocol has noted that “the funding rate of the delta-neutral position will be automatically distributed to stakeholders of the UXD Protocol”.

First, a few definitions/reminders.

- the “funding rate” refers to the yield generated through UXD’s underlying delta-neutral position, and is determined by the price of Perpetual Futures on exchanges such as Mango Markets. This yield can be positive or negative depending on market conditions.

- Since funding rates can be a source of cash or an expense for UXD Protocol depending on if funding rates are positive or negative, UXD has an insurance fund, capitalized with ~$57mm, which is used to pay negative funding rates when they occur.

- UXD Protocol “Stakeholders” refers to UXP Governance Token Holders, UXD Stablecoin Holders, and the UXD Insurance Fund.

- The insurance fund also generates yield through asset management strategies (stablecoin LP positions, lending, etc). The combination of the funding rate plus the yield from asset management strategies can be called the Protocol Yield.

With that in mind, the question to be answered is:

What is the relationship between Stakeholders and the Protocol Yield generated from the delta-neutral position?

The answer to this question is the design of the Protocol Fund.

tl;dr — the Protocol Fund Structure

The Protocol Fund will function as follows:

- UXP Governance Token Holders will be required to stake UXP to (i) participate in governance and (ii) receive their share of the Protocol Yield. Staked UXP will be recorded as veUXP, with governance power dependent on the length of locking.

- UXP Governance Token Stakers will act as a backstop to the insurance fund. In the event the insurance fund is depleted, staked UXP tokens will be auctioned off in a manner similar to MakerDAO’s auction mechanism.

- UXP Governance Token Stakers’ split of the Protocol Yield will depend on the Health Ratio of UXD Protocol. The Health Ratio is the sum of (i) the value of the delta-neutral positions (ii) the value of the insurance fund, divided by the total UXD supply outstanding. For example, if there is $100mm in delta-neutral collateral, $50mm in the insurance fund, and $100mm of UXD in circulation, then the Health Ratio = (100+50)/(100) = 150%. UXD Protocol has derived a Target Health Ratio from historical data. The Protocol Yield split will be 50/50 between UXP Holders and the insurance fund when Health Ratio = Target Health Ratio. The split can increase or decrease depending on if the Health Ratio is above or below the Target Ratio. (See formal details in “Appendix: Yield Split” section below).

- Protocol Yield will be distributed using the veRev Yield Distribution model, as described in our previous article.

- UXP Stakers will receive additional staking rewards in veUXP as well, beyond those from the veRev yield distribution mechanism. This emission will decrease over time and is meant to reward early stakers.

- The Protocol Yield due to UXP stakers will be calculated at the end of each week (period subject to change). If the Protocol Yield for that week is positive, then UXP stakers will receive their split of this yield plus their extra veUXP staking rewards noted above. If the Protocol Yield for that week is negative, UXP stakers will only receive their veUXP staking rewards emission.

veRev

VeRev is a novel mechanism that helps solve prioritization of stakers over non-stakers, creates a new “semi-liquid” veToken, lets paper hands exit the governance system, likely has favorable tax implications, and creates a natural demand vector for non-staked UXP. The full mechanism is described in our our previous article.

Community Feedback

The above design structure is a proposal, and UXD Protocol encourages community feedback in our discord. Please drop by to discuss! UXD Protocol has made a dedicated #protocol-fund-discussion channel.

Designing a Protocol Fund

Below, UXD Protocol details the thought that went into designing the Protocol Fund. It is important to share not only the decided upon structure for large design choices such as the Protocol Fund, but also the thought path that brought these structures to light.

When thinking about the answer to this question, there is a hierarchy of design choices that determine the overall Protocol Fund Structure:

- At a high level, what should the roles of each Stakeholder in the Protocol Fund be?

- Where should the yield to each Stakeholder come from? (delta-neutral position, insurance fund yield, etc)

- How much yield should each Stakeholder receive? (a formalized yield split between Stakeholders)

- In what form should yield be distributed? (buyback and burn? direct cashflow dividends? etc)

For each question, this post will give a proposed answer to each of these questions.

- The relationship between UXP Governance Token Holders, UXD Stablecoin Holders, and the Insurance Fund should be as follows:

UXP Governance Token Holders

- UXP Holders are the stewards of UXD Protocol. Their incentives should be aligned with the long-term success of UXD protocol and the stability of UXD stablecoin. The UXP community should be responsible for the asset management of the insurance fund, and should receive yield in return for their work and assumption of risk. “Do nothing” should be a preferred option for insurance fund asset management strategies (to prevent any highly speculative investments) and the minority should have veto powers.

- UXP Holders should act as a backstop to the Protocol Fund, and (as previously noted) UXP Holders will be required to stake their UXP into the Protocol Fund, as veUXP. (The community should help decide the locking lengths and their governance multipliers!). In the event the insurance fund is depleted, staked UXP tokens will be auctioned off in a manner similar to MakerDAO’s auction mechanism.

- UXP Holders should receive some Protocol Yield when it is positive, but not pay Protocol Yield when it is negative (to the extent the insurance fund is still capitalized). However, there may be a penalty for negative yield resulting from Insurance Fund asset management strategies, in order to incentivize safe strategies for existing assets. In this way, UXP behaves like a rolling call option on the Protocol Yield. In order to align incentives (ensure that UXP holders do not mismanage the insurance fund due to the nature of this call option), the % of yield received by UXP stakers will depend on the overall health of the protocol (see Appendix).

UXD Stablecoin Holders

- Put simply, UXD stablecoin holders should be able to spend minimal mental power on UXD Protocol. Similar to how USDC holders do not need to concern themselves with Centre’s corporate operations, UXD holders should be given the option but not the obligation to participate in decentralized governance.

- UXD = Decentralized USDC + UXP incentive. As discussed before, UXD usage will be incentivized (fee rebates, LM, subsidized lending/borrowing rates) with UXP Governance Token. These incentives are the means through which the option to participate in UXD Protocol decentralized governance is given.

- UXD stablecoin should be a pure stablecoin, and should receive no yield. The goal of UXD stablecoin is to act as a monetary instrument, not a speculative one. This greatly simplifies platform integration (no need for rebasing, airdrops, etc), allows for sufficient liquidity (no need to stake UXD for yield), and helps prevent yield speculation (disentangles UXD from the decentralized interest rate derivatives market that UXD Protocol believes will grow large over time).

UXD Insurance Fund

- UXD Insurance fund exists for the benefit of UXD stablecoin holders, in order to help preserve the stability of the stablecoin. It should be deployed in low risk asset management strategies and generate sustainable yield through positions. Decisions should center around this principle.

- Appropriate safeguards should be put into place to ensure that asset management decisions made by the community of UXP Stakers are aligned with both the protocol and UXD holders. Strategies should be low risk, and thoughtful. Risky strategies should be veto-able, and negative yielding strategies should likely come with some penalty.

2. Where should the yield to UXP stakers come from?

- As the stewards of UXD Protocol, UXP stakers should receive interest from both the delta-neutral position and the insurance fund yield strategies. The former can be interpreted as a “operations fee”, that allows the community to continue to operate, and the latter as an “asset management fee”. Longer term, UXP Stakers may be able to generate incremental yield through other services (for example, potentially through a lending AMO).

3. How much yield should each Stakeholder receive?

- UXD Protocol exists for the benefit of UXD stablecoin holders, and as such the priority should be ensuring the stability and robustness of the stablecoin. As such, yield should be split between stakeholders in a manner consistent with this philosophy.

- Ideally, there would be a principled way to decide the yield split between the Insurance Fund and the UXP Stakers that would reward UXP Stakers for a “healthy” protocol (one where UXD stablecoin holders feel comfortable in their position). Although not perfect, UXD Protocol borrowed the concept of “Value-At-Risk” or VaR from traditional finance in order to determine whether or not the protocol is “healthy” (see Appendix for exact details). In one sentence, a healthy UXD Insurance Fund is large enough to ensure that the probability of insurance fund depletion is ≤10% using historical data and assumptions. This parameter is subject to change.

- Finally, UXD decided on a certain functional form for this yield split (namely a logistic function of the protocol’s health, centered at the “Target

Health Ratio” of the protocol). The key parameters of this function can be determined through governance.

4. In what form should yield be distributed?

- Recently, UXD was excited to share its veRev Yield Distribution model. Although the veRev model was shared generally so that other protocols may adopt the mechanism if they wish to do so, it was designed for the purpose of distributing yield to UXP Stakers.

- The model can be summarized as follows: Periodically (anticipated to be biweekly, every two weeks), UXD Protocol will account for all Protocol Yield earned by the protocol over that period. If this amount is positive, it will be awarded to veUXP stakers in the form of additional veUXP. UXD Protocol will then initiate a Reverse Dutch Auction to offer to buyback veUXP from stakers. Residual cashflow (that is, if the auction does not fill) may be used to buyback UXP on the open market. See the veRev article for a detailed explanation.

- veRev is a novel mechanism that helps solve prioritization of stakers over non-stakers, creates a new “semi-liquid” veToken to help incentivize longer vote-locking, lets paper hands exit the governance system, may have favorable tax implications, and creates a natural demand vector for non-staked Token.

Combining the above parts:

- UXP Stakers are the stewards of UXD Protocol, including the Insurance Fund which exists for the benefit of UXD Stablecoin holders.

- UXP Stakers should be rewarded for their backstopping of risk as well as work to manage Insurance Fund assets.

- The amount of Protocol Yield UXP Stakers should receive relative to the insurance fund should be a function of the Health of UXD Protocol, meaning the level of comfort UXD stablecoin holders feel when holding their position.

- UXP Stakers will stake for veUXP and receive yield using the veRev yield distribution model.

As always, if you’ve made it this far, thanks for reading.

Cheers.

Risk disclosure: All decentralized stablecoins carry risks related to their usage and price stability. Please review UXD Protocol’s Risks section in the docs for more information on potential risks. All design specs above are preliminary and subject to change. Receipt of “yield” may be subject to applicable laws and regulations, including restriction of certain jurisdictions.

Appendix: Technical Specs

As defined above, Protocol Yield (r) will be a combination of asset management strategy yield (r_I) and Delta-Neutral yield (r_DN):

Yield split between UXP stakers pro-rata and the insurance fund will be a function of the overall health of the protocol at a given time, known as the Health Ratio at time t:

The Health of the protocol will be a moving average of the Health Ratio for the past n blocks:

Using historical data, we can calculate a “Value At Risk” Health, which represents the Health value which would cause the protocol to stay solvent in ≥90% of historical scenarios (meaning if UXD protocol began on a random date in the historical data, the probability of bankruptcy is ≤10%.) Note this is the initial parameter chosen and may be subject to change.

Call this value

(essentially this is the “Target Health Ratio” above in the article).

The yield split between UXP holders and the insurance fund is then given by a logistic function:

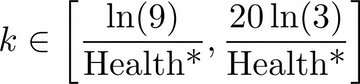

Where r is the total yield generated by the protocol as above and k is a parameter that can be chosen by governance, but must fall in the range:

which was chosen so that

and

which means that k is set such that UXP holders can get 75% of the yield at the quickest if Health_t = 1.05Health* (i.e. current health is 5% above target health), and UXP holders can get 75% of the yield at the slowest if Health_t = 1.50Health* (i.e. current health is 50% above target health).

Indeed the parameter k governs the steepness of the logistic function around Health* (and so can be interpreted as the risk adversity of the UXP stakers, higher k means more risk and more reward, lower k means lower risk and lower reward)

For example, the below is a family of logistic functions with Health* = 1 and k in the above range. The idea is that a larger k is beneficial when the protocol is in favorable health (Health_t above Health*), and highly detrimental when the protocol is in bad health (Health_t below Health*), as the yield decays to zero quickly. The two red curves are the bounds of the family of curves (k at endpoint value of ln(9) and 20ln(3))

Note that, the yield split is always 50% at the Health* optimal value, and increases with varying slope from there.

“k” will be allowed to be changed only once per quarter (subject to change in periodicity), so that there isn’t abuse of the governance system.

Note the final functional form of the yield split will likely include a non-continuous drop-off in yield split if Health is below 100% (the entire protocol is undercollateralized), likely to zero.